Boom to Bust: Memory Makers Plan to Cut NAND Flash Production

by Anton Shilov on April 26, 2019 1:35 PM EST

A true cyclical market, the NAND flash business goes through periods of booms and periods of busts. Following a very profitable boom year in 2018, it looks like the market is in a down swing, as an oversupply is starting to impact the bottom lines of memory makers. To stem any potential for significant losses or an outright market crash, three major manufacturers of NAND memory — Intel, Micron, and SK Hynix — have announced that they will be taking measures to address the oversupply, such as reducing flash production, cutting down wafer starts, and/or slowing down ramp ups of new fabs. Furthermore it is highly likely thr another major manufacturer, Samsung, will follow suit.

The rapid transition to high-capacity 64-layer and 96-layer 3D NAND memory devices has enabled NAND flash manufacturers to increase their NAND supply (as measured in bits) and ultimately saturate the market with loads of flash memory. Meanwhile, demand for servers in the recent months has been weaker than expected, smartphone replacement cycles are getting longer, and other drivers of NAND demand have also disappointed. As a result, NAND supply has well exceeded demand, causing prices to fall by as much as 20% across multiple categories in Q1 2019, according to TrendForce. To ensure their short-term and long-term profitability, at various points in the last couple of months the three manufacturers have all announced that they are taking actions to minimize their exposure during this latest bust.

Micron said back in March that it was carefully managing its NAND bit supply growth (to tackle oversupply at least partially) and started to decrease its total NAND wafer starts by roughly 5% by cutting its legacy nodes. The company did not indicate plans to shrink its NAND bit supply, but reducing production of memory using older process technologies will likely lower its costs.

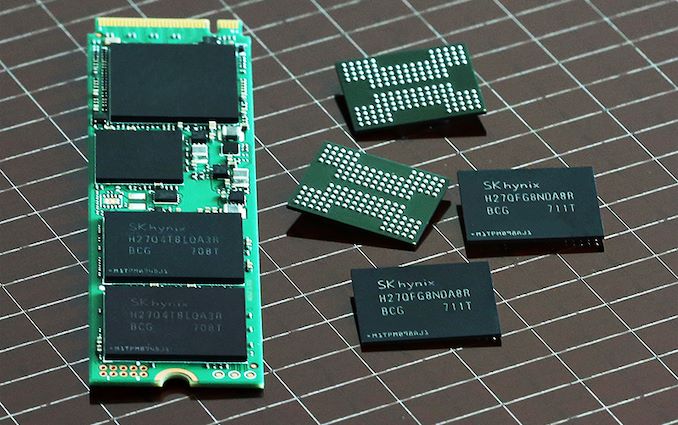

Meanwhile SK Hynix this week said that it had stopped production of 36-layer as well as 48-layer 3D NAND memory, which these days has a rather high per-bit cost relative to newer technologies. In the coming months the company plans to increase production of 72-layer 3D NAND and in the second half of the year it intends to release 96-layer 3D NAND solutions for the SSD and mobile markets. Furthermore, SK Hynix will slow down the ramp up of its M15 fab in Cheongju, South Korea. The company expects its NAND wafer output to decrease more than 10% compared to 2018. Just like Micron, SK Hynix does not seem to have plans to lower its NAND bit production, so it will still more memory than it did last year.

Intel, which has traditionally concentrated on the enterprise part of the SSD market, has also announced this week it will reduce its NAND output in 2019. Intel did not elaborate whether it intended to reduce the number of wafer starts, or do something more radical. But regardless, the company continues to expect challenges with prices of NAND memory going forward, and is acting accordingly.

Finally, while Samsung yet has to announce its Q1 2019 results, it has already warned investors that its profits for the quarter would be down 60% compared to Q1 2018. Analysts have been attributing this to multiple factors, including demand for flagship smartphones, lower prices of DRAM and NAND memory, and other weak markets. Given that the other major memory manufacturers are all taking steps to address the current oversupply, It is more than likely that Samsung will also adjust its NAND business this year; though how they'll do so remains to be seen.

Related Reading:

- SK Hynix Set to Build a New Memory Fab

- SK Hynix to Build a New NAND Fab, Upgrade Existing DRAM Fab

- SK Hynix to Start Using 2nd Gen 10nm DRAM Process Technology in 2H 2019

Sources: Intel, SK Hynix, TrendForce, Micron/SeekingAlpha, Samsung

57 Comments

View All Comments

Anton Shilov - Friday, April 26, 2019 - link

The framework of the story was limited to Q1, when prices of NAND memory decreased by 20%. They predicted one thing, turns out it was inaccurate and they have to respond somehow.brakdoo - Sunday, April 28, 2019 - link

Well, i can read and you should read your first paragraph too. The scope is clearly about the "very profitable boom year in 2018" coming to an end and the companies reaction by reducing output..And when you talk about micron and say "The company did not indicate plans to shrink its NAND bit supply" then you must be crazy if you knew that they did that exactly one quarter earlier...

Also, WDC reduced wafer starts in FY 19 Q1 that will reduce bit output starting FY Q3 (march quarter 19).

AT claims to be "better" than other sites but you are not too far away from wccftech...

Alistair - Friday, April 26, 2019 - link

The Xbox 360 to Xbox One went from 256MB to 8GB memory. 32 times more for the same price. A 20 percent decrease in price in nothing, since it gets cheaper to make the same capacity. We need a huge crash, with all ram prices dropping by 50 percent at least, to be even close to having half the progress of the previous 7 years.Stochastic - Friday, April 26, 2019 - link

The 360 had 512 MB of GDDR3, but yeah...the jump in memory size last generation was massive. The big jump with the upcoming gen is going to be with the CPU (Jaguar to Zen 2 cores) and storage (5200 RPM hard drives to blazing fast SSDs).Tams80 - Saturday, April 27, 2019 - link

We need these companies to stay in business, otherwise there will be no one to make the NAND, let alone develop new NAND.coburn_c - Saturday, April 27, 2019 - link

Oh boy. Idling supply to inflate prices is bad economics. You do pass some costs off onto power distribution and manpower, but your ROI on equipment investment suffers. Why not just try to move more units at a lower margin? This is bad economics. Fucking China.edzieba - Saturday, April 27, 2019 - link

Because negative margin loses you money, and there are per-wafer costs as well as setup costs.This is how demand scaling operates across all manufacturing and how it has done for longer than IC production has existed. The NAND market alone has gone through this cycle many, many times. Waiting of armchair economists is not going to change for industry operates.

FunBunny2 - Saturday, April 27, 2019 - link

"This is how demand scaling operates across all manufacturing and how it has done for longer than IC production has existed. "oddly, of course, econs say price is driven by marginal cost (materials, labor, mostly), while the MBA class say it's average cost (materials, labor, all fixed cost). it's that last the messes things up. IC production is largely fixed cost, since the buildings and machines are being amortized. the only way to do that, and keep average cost under control is to *increase* production. but you can only get away with that if there's also *increasing demand* for your product. since ICs are just intermediate goods in some consumer product, the IC vendor is in a bind with regard to demand. a rock and a hard place. by driving up the cost to the consumer product vendor they end up hurting demand for that product. the IC vendor's average cost goes up, compelling it to raise price further. what's that snake that eats it's tale?

eastcoast_pete - Saturday, April 27, 2019 - link

I really hope that at least one of the agencies charged with ensuring real competition will launch an investigation into price-fixing by this trio of market-dominating memory makers. This almost perfect synchrony of production cuts has the strong smell of illegal coordination with the intent to manipulate the NAND market attached to it.FunBunny2 - Saturday, April 27, 2019 - link

"I really hope that at least one of the agencies charged with ensuring real competition will launch an investigation into price-fixing by this trio of market-dominating memory makers."with regulatory capture in the USofA at a level not seen since Harding, good luck with that.